What’s The Right Mortgage for Me?

Buy a Home

Get the financing you need to turn your dream home into a reality and finally own the house you’ve always wanted.

Let’s Go

Refinance

Adjust your rate or term to suit your needs. Let’s work together to find the best option for you and your financial goals.

Let’s Go

Access Equity

Access your home’s equity to fund improvements, consolidate debt, or achieve your goals.

Let’s Go

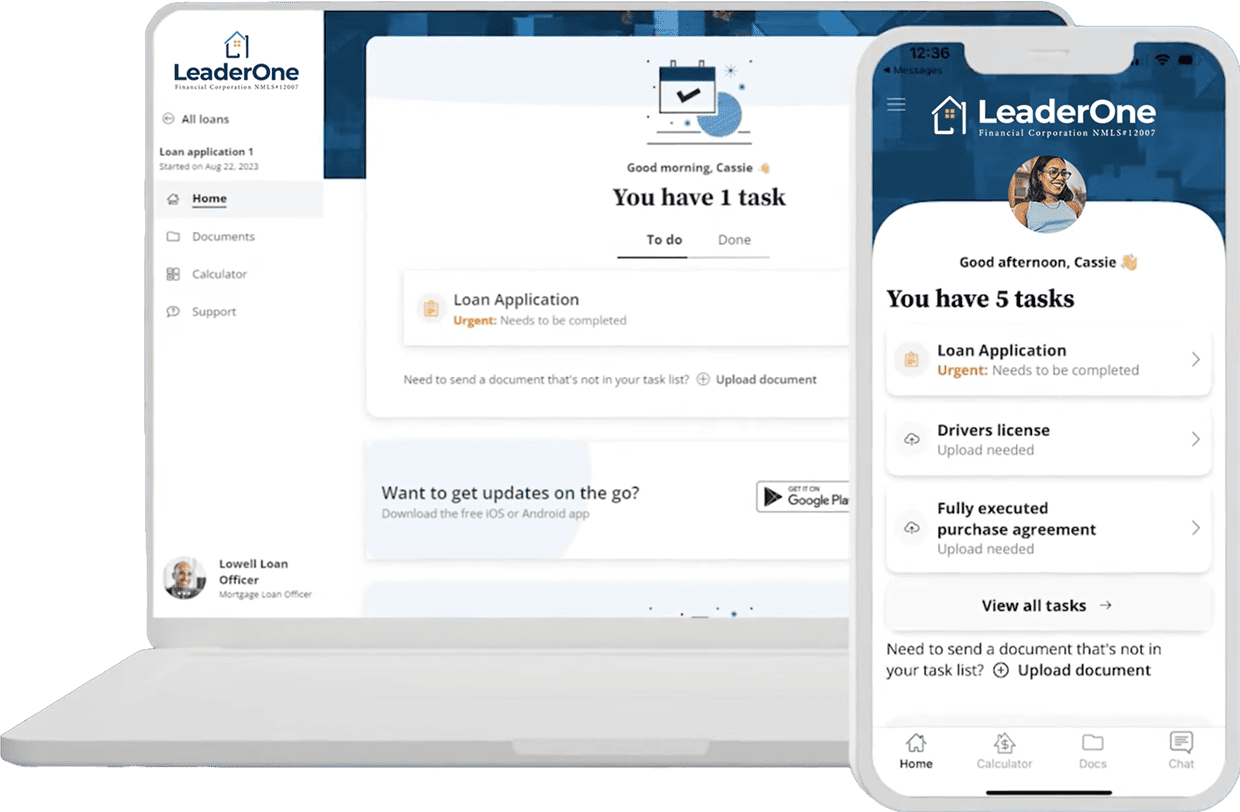

Your home loan journey, right from your phone

The LeaderOne App makes getting started simple. Begin your application, securely connect your income and employment information, and complete verification—all from your mobile device. Everything syncs seamlessly, giving you a clear path forward while your LeaderOne loan partner guides you each step of the way.

Your information is protected with industry-leading security, matched to the right loan options, and moved quickly from application to approval. No pressure. No obligation. Just a smarter, smoother way to move home.

Our results and customers speak for themselves

“Shane and his LeaderOne Financial team are an absolute pleasure to work with.Not only are they professional, highly communicative and extremely reliable, Shane and his team go above and beyond to ensure that each client’s needs and expectations are not only met, but exceeded!

Each member of this team are highly skilled in their respective roles and all have one common goal; to provide unparalleled service to their clients.We confidently refer our real estate clients to their group.”

Realtor Review:

Paige McLaughlin, RE/MAX Alliance

Our results and customers speak for themselves

“LeaderOne is by far the best company I have worked for in 15 years of originating with two other companies. Tremendous support team, for checks and balance and getting the job done.

This company’s support allows me to do what I do best — originate loans. No smoke & mirror here, authentic, real.”

Employee Review:

Team Member, LeaderOne Financial

Our results and customers speak for themselves

“Samson Young is outstanding! Knowledgeable in finance, his guidance saved us $90K — thank you, Samson! Smart, personable, trustworthy!”

Client Review:

— Mary A.